|

The letters and postcard reproduced below were received in response to a completed Independent Foreclosure Review form submitted on January 15, 2012.

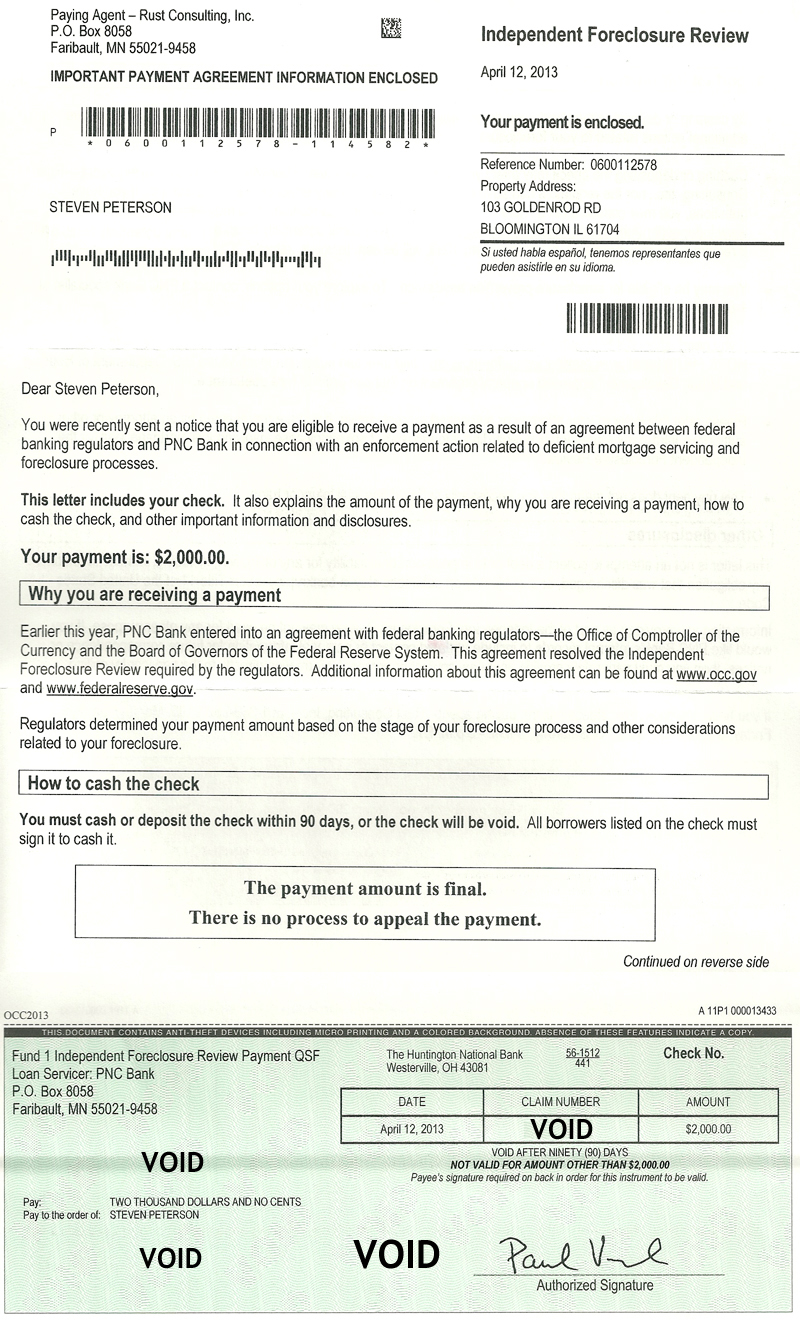

We have elected to post these letters, and the postcard, to commemorate the "official" end of this process. It took 120 days for PNC Mortgage to initiate foreclosure proceedings following the end of our participation in the HAMP program. Thus far, we have received a $2,000 check from the negotiated settlement the OCC brokered with this financial institution. We lost about $25,000 -$30,000 in equity on the house, which PNC has kept for their own purpose (note: this is on top of the principle balance of the loan and the normal interest/profit collected over 6.5 years). If you receive any meaningful response in the course of your foreclosure review, please retain it for the historical record, and consider posting it on the web.

Take Action Today! Use our free template to document your foreclosure and send it to the Senate and House.

|

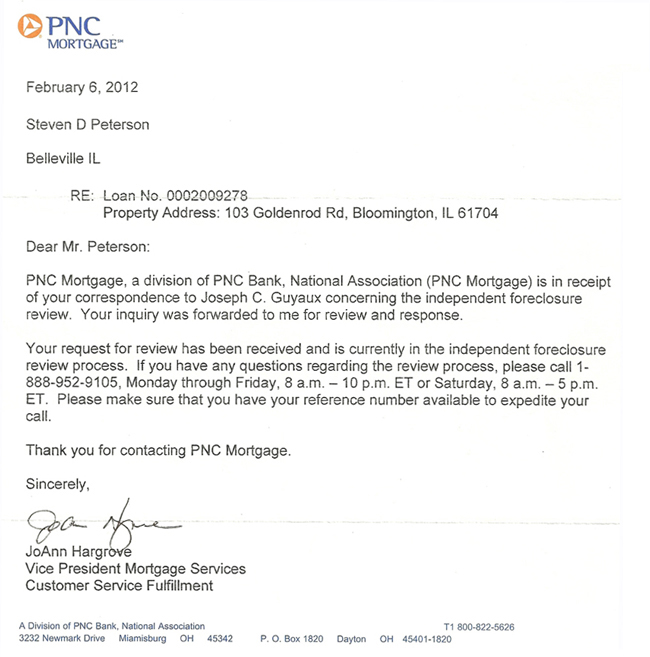

Received three weeks after submitting the review form:

Received nine months after submitting the review form:

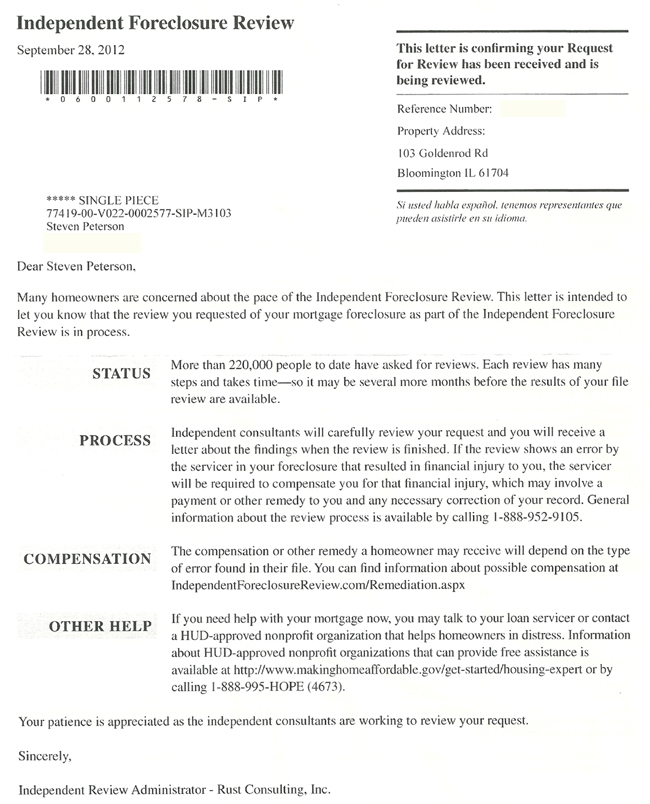

Received fourteen months after submitting the review form:

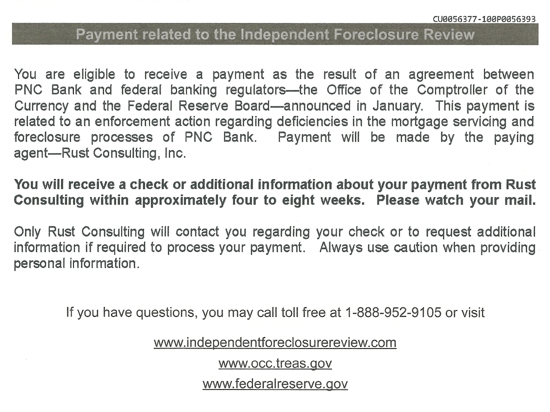

Received fifteen months after submitting the review form:

Final Settlement Check (click images to view full size)

|

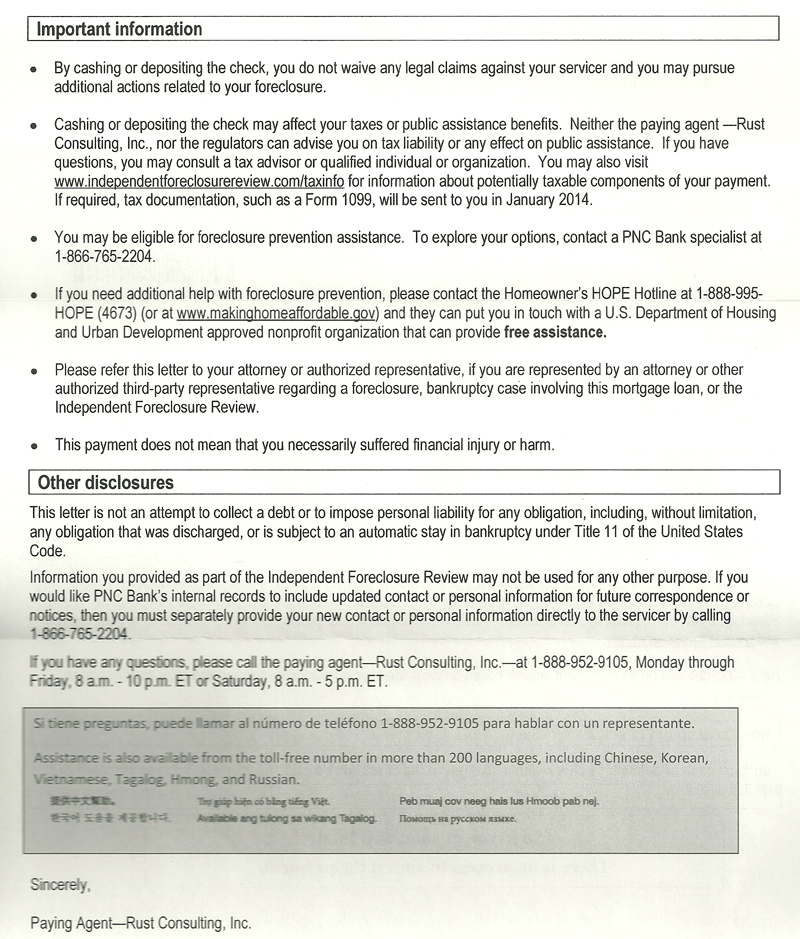

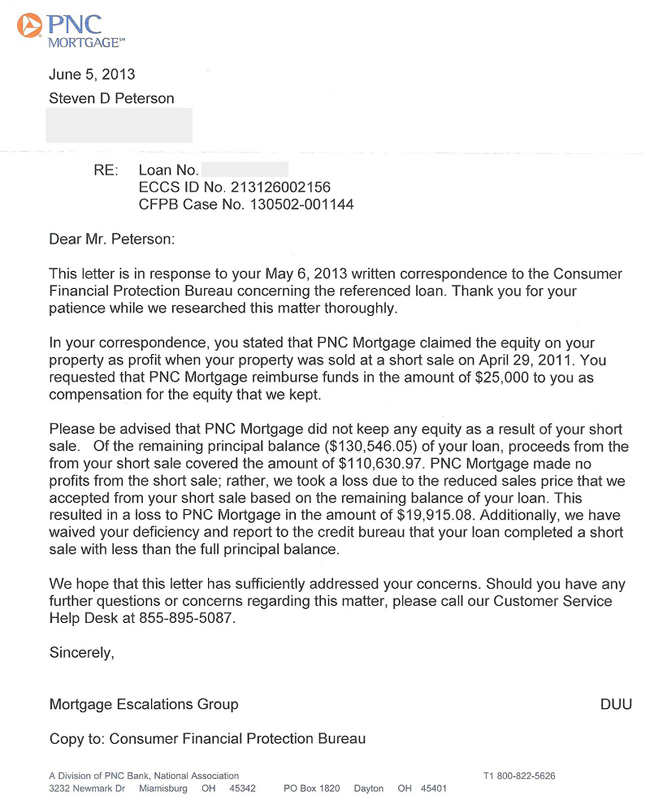

Update! After filing a formal complaint in the CFPB database (a "Request for Disgorgement"), PNC offered the following response. Obviously, they did not expend much effort, or consider the argument we presented in the complaint from any angle that might acknowledge the costs associated with their normal way of doing business.

Following their response, you will find the comments we included in the form used to dispute the response to the complaint. If we receive any response, we will post it for general consideration. |

PNC response to our Request for Disgorgement:

|

Our Reply (filed as a dispute on 06/05/13): In my complaint, I pointed out that PNC collected $202,000 on a $144,000 loan over 6.5 years, including the proceeds from a "short sale." They are claiming a $19,000+ loss on the exchange. It is hard to see this as anything other than an example of a misleading and self-serving accounting practice. Their response does not address the gain in any meaningful way. In my complaint, I at least tried to address the situation from the bank's perspective. PNC does not, however, seem to be interested in responding to events from a customer's point of view. In fact, their response seems to offer an example of a straw man or epistemic argument (i.e., the balance of the loan was not paid in full after the house was sold, therefore PNC lost money on the sale). In their response, PNC does not address the larger equation: a bank may lend $144,000, take in $202,000 in return over 6.5 years, and still claim to have suffered a loss on the deal. This response also offers an example of an argumentum ad consequentiam (argument from consequences): they are offering a premise that asserts negative consequences (a financial loss) from a course of action (a short sale) in an attempt to distract from the initial discussion (is PNC entitled to all proceeds from the sale?). They simply claim a loss without responding to the question posed in the complaint, which is formally titled a "Request for Disgorgement" for a reason. If PNC wishes to maintain their clumsy response to this request, it will not bode well for their branding efforts, as this line of "argument" will become public. After requesting additional time to research their response, I am disappointed that they could not find a more suitable response to the substance of the complaint. If the CFPB could present this dispute to PNC, and allow for a better response to my request, I would be obliged. Thank you for all your efforts on my behalf. Regards, Steven Peterson |