|

The current president and CEO of the Mortgage Bankers Association, David Stevens, has gone out of his way to start a blog, Capital View, where he shares his thoughts "on the intersection of Washington, DC and the Industry." Most of the content posted in Capital View is fairly benign - he comes out in favor of credit monitoring, recognizing diversity, and giving the GSEs a facelift, that sort of thing. Recently, Mr. Stevens posted a piece on the CFPB Complaint Database. He's against it. If I were speaking out on behalf of an industry that recently swallowed the life savings of a few million people, I would probably find the CFPB site a little frightening, too. In response to the essay, I tried to post a comment. There are a few other comments posted, and he seems open to airing an opposing view or two. For whatever reason, the comment remains in limbo, "awaiting moderation." |

|

Of course, Mr. Stevens has no obligation or duty to give my point of view any "airspace" on his blog. He may exercise his editorial authority in any way he chooses. By the same token, I am at liberty to post my response to his thoughts on this web site. That is the beauty and power we may find in our constitutional right to free speech.

In that spirit, I will post my response to Mr. Steven's argument below:

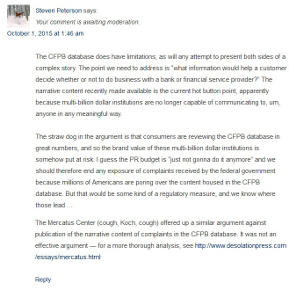

The CFPB database does have limitations, as will any attempt to present both sides of a complex story. The point we need to address is "what information would help a customer decide whether or not to do business with a bank or financial service provider?" The narrative content recently made available is the current hot button point, apparently because multi-billion dollar institutions are no longer capable of communicating to, um, anyone in any meaningful way.

The straw dog in the argument is that consumers are reviewing the CFPB database in great numbers, and so the brand value of these multi-billion dollar institutions is somehow put at risk. I guess the PR budget is "just not gonna do it anymore" and we should therefore end any exposure of complaints received by the federal government because millions of Americans are poring over the content housed in the CFPB database. But that would be some kind of a regulatory measure, and we know where those lead ...

The Mercatus Center (cough, Koch, cough) offered up a similar argument against publication of the narrative content of complaints in the CFPB database. It was not an effective argument - for a more thorough analysis, see:

http://www.desolationpress.com/essays/mercatus.html

Print: |

|

|

|